- The Pulse Newsletter

- Posts

- Signs of Life in Toronto Condo Market

Signs of Life in Toronto Condo Market

MIC Lender cancels redemptions, Canada/Alberta carbon pact, Fed Chair transition

Marc Beavis

May 18, 2026

In partnership with

To our Canadian subscribers; Happy Victoria Day weekend. I hope you’re enjoying the extra day of rest and activities. The stories I’ve included in this week's edition look at housing (the good and the bad), energy policy and the fight against inflation, and the room for easy decisions is narrowing. I hope you enjoy the read.

Market Recap: U.S. and Canada

It was pretty rough going early in the week, with sharp early declines across the board on Tuesday before a strong midweek recovery pulled most markets back into positive territory. Friday brought renewed selling pressure that erased much of those gains, and that left three of the four benchmarks modestly in the red. Tech showed the widest swings, dropping more than 2% intraday Tuesday before recovering by Thursday.

As for the numbers, the S&P 500 led the week with a gain of 0.13%, followed by the Dow Jones at -0.17% and the Nasdaq 100 at -0.38%. The TSX lagged, finishing the week down 0.72%.

Week ending May 15, 2026

Major Economic Stories This Week

US Inflation Climbs To A Two-Year High

Annual CPI rose to 3.8% in April, the highest reading since May 2023.

The war in Iran continues to push energy prices higher, and that pressure is now spreading well beyond the gas pump. Energy is doing the heavy lifting on the headline number, but the monthly print shows broader pressure building, with shelter, food, and transportation costs all firming up. The monthly pace eased a bit from March, which, on the surface, looks like progress, but only when compared to what was the hottest monthly inflation reading in nearly four years. For the incoming Fed chair, this is the kind of report that closes the door on near-term rate cuts.

April CPI forecast: 3.7% — actual print of 3.8% came in above expectations

Energy contribution: prior month annual gain was 12.5% — April's 17.9% reflects continued acceleration

Shelter annual pace: up from 3.0% in March — the largest single-category driver outside energy

Monthly CPI: in line with consensus expectations — first time forecasts have been met in three months

Core Inflation Joins The Move Higher

Core CPI accelerated to 2.8% annually in April, with monthly prices rising 0.4%.

This is the print that should concern the incoming Fed chair more than the headline number. Core inflation strips out the volatile energy and food categories, which means it reflects domestic pricing pressure that has nothing to do with the war or oil markets. Services excluding energy are now the primary driver, with shelter and transportation services leading the move. The monthly figure jumped to its sharpest single-month gain since early 2025, and that’s a material step up from the steadier pace of February and March. The energy shock is now bleeding through into services, which is exactly the dynamic central bankers worry about most.

Core CPI forecast: 2.7% — actual 2.8% reading exceeded expectations

Monthly core forecast: 0.3% — actual 0.4% reading also came in hot

Apparel: +4.2% annually — a category typically more responsive to discretionary demand than necessity

Used vehicle prices: -2.7% — one of the few categories providing meaningful disinflationary offset

Wholesale Prices Post Biggest Monthly Jump In Four Years

Producer prices climbed 1.4% in April, the largest monthly increase since March 2022.

If CPI tells us where prices are today, PPI tells us where they're heading. April's wholesale data was bad across the board. The headline number posted its biggest monthly jump in four years, with both goods and services contributing in a big way. Wholesale gasoline drove much of the goods weakness, but the services side told the more important story, with the biggest monthly services PPI gain since early 2022. That kind of pipeline pressure typically takes several months to fully filter into consumer prices, which means CPI prints through the summer are likely to remain elevated regardless of what happens at the gas pump.

PPI forecast: 0.5% monthly — actual 1.4% reading came in nearly triple expectations

March PPI: revised upward to 0.7% from initial estimate — trend was stronger than first reported

Annual PPI forecast: 4.9% — actual 6.0% print well above consensus

Categories with rising costs: jet fuel, diesel, industrial chemicals, freight transportation, legal services — pressure is broad-based

TOP INSIGHTS

Inflation Is No Longer Just An Energy Problem

Last month, you might have reasonably argued that the inflation spike was a one-month event driven entirely by oil. This month though, that argument falls apart. Core CPI accelerated to 0.4% monthly, services less energy services hit 3.3%, and transportation services climbed 4.3%. The pass-through from higher energy costs into the broader services economy has begun in ernest, and that's a significantly different problem than a simple gasoline shock.

The pain is now shifting from the gas pump to almost everything else. Rent, insurance, dining out, doctor visits, airfare; you name it. These categories don't reverse easily even when oil prices eventually normalize, because once businesses raise prices to cover higher input costs, they rarely roll them back. The lived inflation experience is about to get worse before it gets better, and the gap between official statistics and how people actually feel about prices will keep widening.

I expecting that the next two or three prints will continue showing this broadening pattern. The window where the Fed could plausibly call this transitory has effectively closed. If services inflation stays at this pace through summer, the rate cut conversation moves from just delayed, to off the table for 2026.

Real Wages Just Flipped Negative Again

The most important number this week, as I see it, can’t actually be found in the reports listed here, but I felt compelled to include it in this week’s Top Insights section. If you read the last story in this edition, discussing new Fed Chair Kevin Warsh, you’ll note the comparison of CPI to wage growth. Average paychecks grew 3.6% over the past year while prices rose 3.8%. That gap ends a three-year stretch where real wages were positive, meaning wages were keeping pace with or outpacing inflation. Real wage growth is the single best predictor of household discretionary spending capacity in the months ahead, which makes this shift more consequential than most market commentary is acknowledging.

When real wages turn negative, household behaviour changes fast. Big-ticket purchases get deferred, savings get drawn down to cover essentials, and consumer confidence erodes. Whirlpool already described demand for major appliances as "recession-level." And that’s the pattern you'd expect when household real income is shrinking. The retail sales gains we're seeing are coming from higher prices rather than higher volumes, which is a hollow form of growth that doesn't support corporate earnings the way real demand does.

I’m betting this dynamic gets worse before it gets better. Wage growth responds slowly to inflation while consumer prices respond quickly, so the gap is likely to widen further if headline CPI stays above 3.5% into the summer. Markets still seem comfortable with the consumer story for now, but the household economy is showing strain that doesn't fit a bullish scenario. This is the variable I'd watch most closely heading into Q3 earnings season.

Warsh Inherits An Unwinnable Setup

Kevin Warsh takes over the Fed on Monday into the worst possible inflation backdrop. Headline CPI is accelerating, core CPI is reaccelerating, PPI just posted its biggest monthly jump in four years, and the president who appointed him has been very public about wanting lower interest rates. The math says hold. The politics say cut. There is no version of this setup where Warsh looks good in the first six months on the job.

For the markets, the takeaway is that the Fed cannot move regardless of who runs it. Cutting rates into a 3.8% headline CPI with services prices firming would be a clear policy error. The "Fed pivot" trade many investors have been positioned for keeps getting pushed further out the calendar.

I think Warsh holds through at least mid-year, and likely longer if services inflation doesn't break. He has every incentive to establish credibility early, and cutting into this data would do just the opposite. Another interesting tension is whether political pressure starts to threaten institutional independence in more visible ways. That's the bigger risk story for markets in my view. Not the rate path itself, but the growing perception that the Fed may no longer be making decisions purely on data.

The 10 Best AI Stocks to Own in 2026

AI is moving from experiment… to essential.

Every major industry is integrating it.

Every major company is investing in it.

By late 2025, AI was already an $800B market — growing at a pace that could push it well beyond $1 trillion in the years ahead.

Cloud infrastructure is scaling fast.

AI-enabled devices are multiplying.

Automation is becoming standard.

But here’s the real question…

When trillions flow into this transformation — which stocks stand to benefit most?

Our new report reveals 10 AI stocks positioned across the backbone of this shift — from the companies powering the infrastructure… to those embedding intelligence into everyday systems.

If you want exposure to one of the defining growth trends of this decade, start here.

TOP STORY

Has Toronto's Condo Market Hit Its Bottom?

Sales climb 14.4% year-over-year as buyers return

Average condo prices still down 6.4% from last year

Lower rates and falling prices unlock first-time buyers

Investor exodus forces developers to focus on end users

Toronto's condo market is showing the clearest signs of life it's had in over a year. After months of cancelled projects, expanding inventory, and sellers reducing prices with no offers in sight, new data from the Toronto Regional Real Estate Board points to a market that may have finally found its floor. Buyers are returning, motivated by lower borrowing costs and prices that look more like 2017 than 2022.

A Buyer's Market Takes Shape

Realtor Thomas Delespierre says the segment has shifted from a seller's market, where units sold in under two weeks, to one where condos can sit for four to six months. Buyers now have choice and leverage. TRREB's chief information officer Jason Mercer pointed to sidelined buyers re-entering the market as affordability improved. Greater Toronto Area condo prices have dropped roughly 25% from their 2022 peak, and the pattern extends to most surrounding suburbs and other major Canadian cities.

The Supply Question Looms

At least nine condo projects in Toronto were cancelled in 2025, and developers like Daniels Corporation have scaled back from eight to ten active projects to just four. With investor buyers having fled the market, developers are reorienting toward end users, building larger units and fewer studios. Mercer warned that thinner new supply could push prices back up once existing inventory clears. The question now isn't whether demand recovers, but rather whether builders can deliver enough product to meet it without prices running away again. This should be interesting.

Read the full story here.

As I cover in today’s top story, Toronto's condo market is showing signs of a bottom. Sales climbing and buyers are returning as prices and borrowing costs ease. But the recovery isn't uniform across property types, and the right entry point depends heavily on what you're buying and where. For first-time buyers especially, the trade-off between affordability, space, and commute has rarely been more pronounced.

Please vote on this week's question:

What's the smarter first-time buyer move? |

LAST WEEK’S POLL RESULTS

In our last poll, I asked whether Berkshire Hathaway's share price would outperform the S&P 500 over the next five years. 42% said yes, Abel will be ok, 39% felt it was too early to judge, and 19% thought the Buffett premium would disappear. A clear lean toward confidence in the post-Buffett era, although a meaningful share of readers are reserving judgment. Thanks to everyone who voted.

READER COMMENTS

Abel will be ok

"I do... Why? It'll have more to do with the S&P 500 underperforming its long-term annualized performance over the next 5 years, than Berkshire blowing the doors off IMO.

With that said, I think some of Berkshire's outperformance could be due to company using chunk of its ~$380B to make needle-moving acquisitions and substantial equity investments. Might not happen this year or maybe not even next, but they'll be ready when opportunities are aplenty.

Won't be surprised at all to see Greg Abel make a push into international acquisitions, while pushing deeper into ex-U.S. equity investments, much like they've done in the past with Japan trading houses in years past as well." - callawayguy

CANADA MORTGAGE CRISIS?

Mortgage Lender Halts Investor Redemptions

Mortgage Company of Canada freezes redemptions and distributions

Rising delinquencies in Toronto region overwhelm the fund

MIC delinquency rate eight times higher than chartered banks

Backlog in Ontario courts delays power-of-sale recoveries

In a possible sign of things to come, Mortgage Company of Canada has paused investor redemptions and distributions for its residential lending fund, becoming the latest private lender to lock the door as housing market stress deepens. The Toronto-focused mortgage investment corporation cited a difficult year of rising delinquencies, in addition to depressed home prices and a court backlog that's slowing the recovery process when borrowers default. For investors who put up the minimum $25,000 to access higher-yield private mortgage exposure, the money is now stuck.

Why The Freeze Happened

CEO Raj Babber described 2025 as "profoundly challenging," with the Toronto region's real estate market remaining weak and home prices still well below their 2022 peak. Losses on portions of the portfolio have been realized faster than anticipated. After the June 15 distribution, income distributions will be suspended entirely, with cash thereafter distributed pro-rata through mandatory monthly redemptions capped at 8% annually of each investor's holdings. The notice didn’t specify how long the suspension would last.

What It Signals About The Broader Market

Mortgage investment corporations had a delinquency rate of 1.96% in Q3 2025, compared to just 0.24% at chartered banks. The gap reflects the riskier borrower profile MICs typically serve, but the trend is what matters here. CMHC has flagged rising delinquencies in general, and this fund's freeze follows a pattern of private debt and real estate funds limiting withdrawals through 2025. Rising unemployment, US trade tensions, and the war in Iran are all weighing on consumer and investor confidence in housing, and that probably means more stress in this corner of the market is likely before things improve.

Read the full story here.

Become An AI Expert In Just 5 Minutes

If you’re a decision maker at your company, you need to be on the bleeding edge of, well, everything. But before you go signing up for seminars, conferences, lunch ‘n learns, and all that jazz, just know there’s a far better (and simpler) way: Subscribing to The Deep View.

This daily newsletter condenses everything you need to know about the latest and greatest AI developments into a 5-minute read. Squeeze it into your morning coffee break and before you know it, you’ll be an expert too.

Subscribe right here. It’s totally free, wildly informative, and trusted by 600,000+ readers at Google, Meta, Microsoft, and beyond.

THE ENERGY SECTOR

Ottawa And Alberta Sign Pipeline Carbon Deal

Carbon price set at $130 per tonne by 2040

Pipeline application due to Major Projects Office by July

Construction could begin as early as 2027

Pathways CCS targets cut from 22 Mt to 16 Mt has proposed an outright ban on prediction markets and a 17.5% fee

Prime Minister Mark Carney and Alberta Premier Danielle Smith signed a long-awaited carbon-pricing and emissions-reduction agreement in Calgary last week, finalizing the central piece of a memorandum of understanding the two leaders forged last year. The deal ties federal support for a new one-million-barrel-per-day pipeline to the Pacific Coast to Alberta's commitments on industrial carbon pricing and carbon capture. It's a material step toward bolstering Canadian energy exports, even though several major hurdles still have to be overcome.

The Carbon Pricing Mechanics

The headline carbon price ramps to $115 per tonne by 2030, $130 by 2035, and stays at $130 through 2040. The guaranteed floor, though, is lower at $110 per tonne by 2040, and officials are describing it as a regulated minimum that markets are expected to push above. This is substantially weaker than the $170-per-tonne by 2030 target the previous Trudeau government had set. Environmental groups including the Canadian Climate Institute said the compromise puts the national net-zero-by-2050 goal out of reach and could weaken policy in other provinces.

What Still Needs To Happen

Alberta must submit its pipeline application to Ottawa's Major Projects Office by July 1, and federal designation as a project of national interest is expected by October 1. Oil could flow as early as 2033 or 2034, although a route remains undecided. First Nations on B.C.'s Northern Coast remain opposed to coastal oil export, and a Trans Mountain-adjacent route to Burnaby is now under consideration. The Pathways CCS project, central to the emissions side of the deal, has had its target cut from 22 megatonnes to 16 megatonnes annually, with only 6 megatonnes required from CCS specifically by 2035.

Read the full story here.

THE FEDERAL RESERVE

Warsh Inherits A Fed In Crisis

New Fed chair takes over Monday into rising inflation

Retail demand softening as households pull back spending

Real wage growth turns negative for first time in years

Services inflation showing signs of becoming sticky

Kevin Warsh takes over as Federal Reserve chair on Monday, replacing Jerome Powell after his eight-year term. The handoff comes two and a half months into a war that has sent consumer prices climbing, and Powell will remain on the board of governors in an effort to defend the Fed's independence. The economic backdrop is brutal for an incoming chair: we’ve got inflation accelerating, consumers are retrenching, and a president who is openly demanding rate cuts. It’s hard to imagine a more challenging scenario for Warsh. There's certainly no clean path forward.

The Consumer Is Cracking

As noted above, retail sales data this week confirmed what CEOs have been flagging for weeks: households are pulling back on big-ticket items and getting more selective on essentials. Whirlpool described the dynamic as a "recession-level" pullback similar to 2008. Gasoline is the primary culprit, with the war in Iran pushing energy costs higher and raising the cost of moving everything else. CNN polling shows 75% of Americans say the war has hurt their finances, and consumer sentiment has hit an all-time low by at least one measure. Retail sales rose 0.5% in April, but most of that reflected higher prices rather than higher volume.

The Sticky Inflation Problem

Wages grew 3.6% over the past year while prices rose 3.8%, meaning that real wage growth has flipped negative for the first time in three years. Services inflation, which tends to be sticky once it firms, is now showing up in both CPI and PPI data. Core PPI rose 1% month-over-month, and wholesale services have posted their biggest gain in four years. As one strategist put it, the Hormuz crisis is aggravating the problem, but the trend goes well beyond oil. Cutting rates into this environment would only make inflation worse, which means Warsh will likely have to disappoint the president early and often.

Read the full story here.

Lululemon says talks with founder Chip Wilson collapsed over escalating demands

Wilson wanted the appointment of three directors chosen by him, including the immediate appointment of two of his nominees and a third from a pool he selected

Globalization gutted Canada’s manufacturing. Here’s how we make things ourselves again

If we act now, we will be a country that can produce far more of what it consumes at a profit

Jury set to deliberate in Musk's lawsuit against OpenAI

Elon Musk, the world's richest person, has accused OpenAI CEO Sam Altman of "stealing" a "charity" and is calling for his ouster from the company's leadership. A parade of wealthy Silicon Valley figures have taken the witness stand over the past several weeks, while protesters outside the courthouse took aim at both sides.

Marketing your bar for the World Cup? FIFA’s strict trademark rules could land you a cease and desist

To get a sense of what the rules around FIFA branding are, CBC News went through its publicly shared intellectual property guidelines and its hosting addendum with the city.

Sheinbaum Backs Reforms to Candidate Selection for Judicial Vote

Mexican President Claudia Sheinbaum will submit a proposal to Congress to reform an upcoming judicial election, following widespread criticism of the erratic rulings of inexperienced judges elected during the first vote last year.

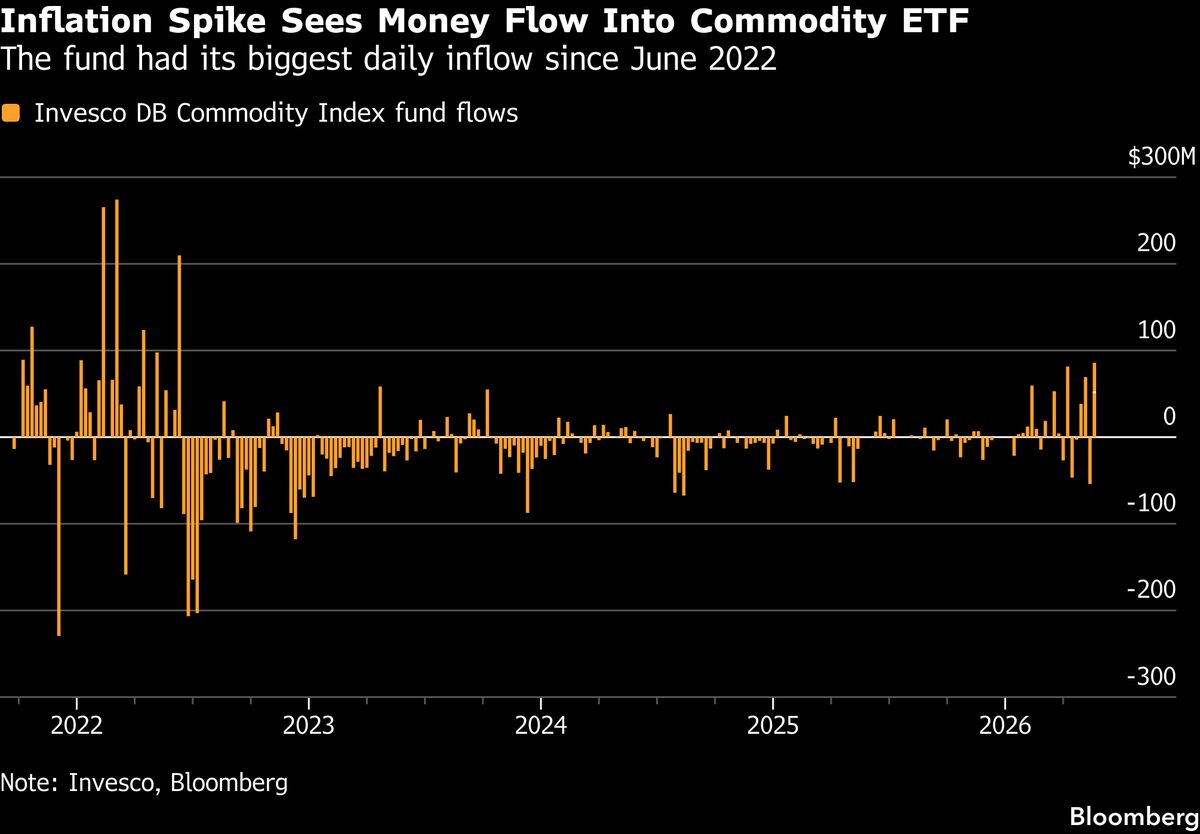

Investors Flock to Commodity ETFs as Iran War Fuels Energy Inflation

Investors are pouring money into commodities funds as the US-Iran war stokes inflation, according to Invesco Ltd.

UK growth forecast upgraded by IMF but risks remain

Growth has been upgraded from 0.8% to 1% for 2026 in the influential body's latest forecast.

Is the UK's once favourite car coming back as an EV?

The company has announced plans to build seven new models in Europe including a small electric hatchback.

‘Michael’ reclaims the top box office spot in its 4th weekend

The Michael Jackson biopic, “Michael,” is reclaiming the top spot in the North American box office

Summer travelers who relied on Spirit Airlines may struggle to find alternatives

The collapse of Spirit Airlines isn't the only curveball confronting people planning summer trips

Week ending May 15, 2026 | Market Cap > $10 Billion USD

Week ending May 15, 2026 | based on 14-Day RSI | Market Cap > $10 Billion USD

The Relative Strength Indicator (RSI) can provide a signal that suggest a stock is either overbought or oversold.

📈A stock that has an RSI over 70 is considered to be in “overbought” territory. This might suggest that the stock is due for a pullback, however it is not a recommendation to sell.

📉A stock that is trading with an RSI below 30 is considered to be in “oversold” territory. This might suggest that the stock is due for a recovery, however it is not a recommendation to buy. Always perform your own due diligence.

Reply