- The Pulse Newsletter

- Posts

- Carney And Sheinbaum Agree To Move Together On Trade

Carney And Sheinbaum Agree To Move Together On Trade

Apple's CEO Switch | Fed Chair's Future | Global Recession Watch

Marc Beavis

April 26, 2026

Sunday brings us another week and another round of things to think about. Canada and Mexico are building an alliance ahead of what will surely be a difficult renegotiation with the U.S., the Apple CEO is handing over the reigns and the war in the Middle East is testing the resilience of the global economy in ways economists are still debating. Let’s break it all down.

Market Recap: U.S. and Canada

It was a bit of a wild week for markets, with tech carrying US indices higher, but it certainly was choppy. The Nasdaq pulled away from the pack on Friday, the TSX spent most of the week in the red, and the Dow & S&P bounced around a bit before finishing relatively flat.

As for the numbers, the Nasdaq 100 led the way with a gain of 2.37%, the S&P 500 posted a modest gain of 0.55% and the Dow Jones slipped 0.44%, The TSX was the week's clear laggard, finishing down 1.29%.

Week ending April 24, 2026

Major Economic Stories This Week

Canada's Inflation Jumps On Energy Reversal

Headline CPI rose to 2.4% in March as energy swung sharply higher, with core inflation edging up to 2.5%.

Once again, the energy story is doing the heavy lifting here. Consumer energy inflation flipped from a deflation rate of 9.3% in February to a gain of 3.9% in March, a byproduct, of course, of the Middle East war’s disruption to global oil supply. That reversal pulled transportation inflation sharply higher and added upward pressure to shelter and recreation costs. On the flip side, food inflation eased as GST/HST base effects continued to work through the numbers. Core inflation's move from 2.3% to 2.5% is modest, but the direction is of note, and the Bank of Canada will be watching whether this is a one-month energy shock or whether it is just the start of a renewed upward trend.

Gasoline: +21.2% monthly, the single largest contributor to the energy swing

Transportation inflation: +3.7% vs -0.8% in February, direct downstream effect of fuel costs

Shelter inflation: +1.7% vs +1.5% in February, modest but moving in the wrong direction

Recreation and education: +2.6% vs +0.5% in February, notable acceleration outside the energy complex

US Retail Sales Spike, But Fuel Is Doing The Work

Retail sales jumped 1.7% in March, the steepest gain in a year, though a 15.5% surge in gasoline station receipts drove much of the headline.

Retail sales jumped 1.7% in March, the steepest gain in a year, though a 15.5% surge in gasoline station receipts drove much of the headline.

Strip out the fuel spike and the picture is still solid, but more modest. Core retail sales rose 0.7%, well ahead of expectations of 0.2%, and gains spread across most categories including furniture, electronics, building materials, and food. Restaurants and bars posted only marginal growth. The broad-based gains suggest consumers remained willing to spend, possibly supported by larger-than-usual tax refunds. The concern going forward is whether fuel costs continue to erode purchasing power. When gas prices stay elevated, we can expect that spending resilience to fade.

Motor vehicles and parts: +0.5%, held up, though well below the headline pace

Food and beverage stores: +0.7%; health and personal care: +0.5%, steady across staples categories

Nonstore retailers: +1.0%, online and direct-to-consumer channels continued to grow

Restaurants and bars: +0.1%, the only service-sector category

US Jobless Claims Remain Low

Initial claims rose modestly to 214,000 for the week ending April 18, with continuing claims edging slightly higher but well below year-ago levels.

The labour market continues to send a calm signal even though there is still a lot of broader economic noise. Initial claims came in close to expectations and are still well below last year's averages, and that reinforces the Fed's repeated observation that firing activity is low. Continuing claims ticked up marginally but aren’t flashing any warning signs. Federal employee claims, which have drawn attention as a proxy for government layoff impact, actually fell on the week to 452.

Four-week trend: both initial and continuing claims remain below prior-year averages, no upward drift

Continuing claims: 1,821,000, up 12,000 on the week, but the level remains historically contained

Federal employee claims: 452, fell by 60, the smallest subset of total claims by a wide margin

Gap to recession threshold: initial claims would need to sustain above roughly 300,000 to signal meaningful labour market stress

TOP INSIGHTS

The Energy Shock Is Now Showing Up In The Data

What stands out this week is how synchronized the inflation signal is across Canada and the US, and how much of it traces back to a single source. Energy drove Canada's headline CPI from 1.8% to 2.4% in one month, just as it distorted US retail sales sharply upward. The Strait of Hormuz disruption is fully being priced into the consumer price data now.

Energy inflation is the most immediate and visible form of price pressure. It shows up at the gas station first, then spreads into transportation costs, food distribution, and services. Monthly CPI gains of 0.9% are the kind of numbers that shape how people feel about the economy regardless of what the core figures say. Consumer confidence tracks the headline number more than central bankers would like to admit.

The key question is duration. If the Strait situation stabilizes in the coming months, both countries will likely look back at this print as a temporary shock. But if oil prices stay elevated through the summer, core inflation will start feeling that pressure too, and the Bank of Canada and the Fed will have less room to maneuvers than markets currently expect. The next two monthly energy readings will tell us a lot.

Retail Resilience Is Real, But The Headline Makes it Look Better Than it Is

The US retail sales number looks impressive on the surface, and the underlying breadth is provides some genuine encouragement. Gains spread across nearly every major category, and core sales beat expectations by a wide margin. Obviously, consumers are still willing to spend.

But as is always, let’s look beyond the headlines. A 15.5% spike in gasoline station receipts inflated the top-line figure a lot. Households spending more at the pump aren’t spending more in a way that reflects confidence or income growth, they’re spending more because the price of a necessity went up. That is a real distinction. Discretionary categories posted respectable but modest gains, and restaurants barely moved. As I say, the picture is solid, but not as strong as the headline implies.

The risk over the next month or two is that sustained fuel costs begin showing up as a drag on the categories that actually reflect consumer health, such as discretionary spending, dining, and entertainment. The tax refund-driven spending we see this time of year tends to be front-loaded in the spring, but if that tailwind fades and pump prices stay high, the retail picture could soften fairly quickly.

A Labour Market That Refuses To Crack, For Now

US jobless claims continue to be one of the most puzzling stories. Week after week, the numbers have been coming in near expectations, well below year-ago levels, and without the kind of upward drift you would expect if the economy were absorbing meaningful damage from tariffs, energy costs, or policy uncertainty.

That is actually the more interesting observation. Let’s not lose sight of the fact that that that we’ve had a disruptive macro backdrop for months. Think trade tensions, an oil shock, elevated rates, federal workforce uncertainty. And yet the private-sector labour market keeps shrugging it off. Federal employee claims specifically fell on the week, which suggests the government restructuring narrative hasn’t translated into the kind of broad job loss some were anticipating.

What I’m watching is whether this holds through the spring. Labour market data tends to lag, and companies slow hiring and reduce hours before they start cutting headcount. The real stress test will come if fuel costs persist and consumer spending softens. Calm data in a noisy environment sometimes just means the lag hasn't caught up yet.

IN PARTNERSHIP WITH HARVEST ETFS

Harvest Income Leaders™ ETFs | Strong Businesses – High Income

Harvest Income Leaders™ invest in leaders that have defined the market here at home and around the world. These are strong businesses that are widely known and have demonstrated their ability to adapt and innovate in their respective industries.

Income Leaders™ target dominant companies. These ETFs offer access to sectoral themes like healthcare, technology, utilities, and more.

Healthcare | Harvest Healthcare Leaders Income ETF (TSX: HHL)

Healthcare stands apart as an essential, diversified, and innovation-led sector. It is underpinned by three permanent, non-cyclical drivers: Aging demographics, technological innovation, and developing markets. Long-term drivers are shared across healthcare sub-sectors, but short-term catalysts may differ. This is why HHL provides diversified exposure.

HHL provides access to a portfolio of healthcare leaders. It boasts a 10+ year history, paying consistent monthly distributions every month over its lifespan.

Technology | Harvest Tech Leaders Income ETF (TSX: HTA)[i]

Technology is a diverse sector with many growth factors. Of course, artificial intelligence remains a significant story. Dominant technology companies have committed hundreds of billions in annual capital expenditures. The value of global IT is projected to exceed US$6 trillion in 2026.

HTA provides exposure large-cap technology companies with a global footprint. It has a track record over a decade old, delivering consistent monthly income. Moreover, HTA has increased its monthly distribution six times since its inception.

Utilities services like lighting, heating, and water, are essential services – available and consumed regardless of market and economic conditions. Owning utilities continues to be a good defensive posture for a portfolio. Utilities is also benefiting from the growth of generative AI, and the surge in energy demand from its use.

HUTL provides investors access to the powerful trends in the utilities space, and monthly income from covered calls.

*See Harvest ETFs Disclaimer at the end of the newsletter

TOP STORY

Canada And Mexico Align Before USMCA Talks Begin

Prime Minister Carney and Mexican President Sheinbaum have agreed to co-ordinate closely ahead of USMCA renegotiations

Canada requested the call, signalling it is actively building alliances before talks formally begin

The US has already been seeking upfront concessions from Ottawa before negotiations start

The USMCA's formal review date is July 1, with talks expected

Canada and Mexico are moving closer together as North America's trade landscape grows more complicated. The two leaders spoke Friday to align on shared economic priorities and formally pledged to co-ordinate their approaches to the upcoming USMCA review. Canada requested the call, apparently, and that says a lot about where Ottawa sees its leverage heading into what its own chief negotiator has warned could be turbulent negotiations.

The Stakes Are High On Both Sides

Mexico has a trade mission to Canada scheduled for early May, led by its Secretary of Economy. That visit will cover Montreal and Toronto, with a possible Ottawa stop still undecided. The timing matters: Mexico already has its first bilateral negotiating round with the US set for May 25, while Canada has no dates confirmed for its own talks with Washington. That asymmetry has drawn questions from Canadian MPs, and the Carney government's answer so far is that Canada stands ready. In addition to the trade file, the two leaders also discussed expanding collaboration in critical minerals, clean energy, and advanced manufacturing, areas where both countries have growing strategic interest independent of whatever the US decides it wants from the table.

What Comes Next

The three-country agreement faces a choice: extend for another 16 years, move to annual reviews, or risk expiry. Any party can also withdraw with six months' notice. The US has signalled it wants concessions before formal talks even begin, and Canada has publicly pushed back on that framing. Whether that posture holds once negotiations get real will define the next several months of North American trade politics, and is also the subject of this week’s poll question.

Full story here.

The USMCA review is now officially underway, and the range of possible outcomes is wide. Canada and Mexico are coordinating their approaches, the US is already signaling it wants concessions, and formal negotiating dates haven't even been set yet. How this plays out will have real consequences for Canadian exporters, workers, and the broader economy. Please vote on this week's question:

What do you think is the most likely outcome of the USMCA review? |

LAST WEEK’S POLL RESULTS

In last week's poll, I asked who you hold most responsible when ticket prices spike for major events. Ticketing platforms took the blame by a wide margin, with 73% of you pointing the finger there, while 19% held artists and venues accountable and just 8% placed responsibility on buyers. Thanks to everyone who voted.

READER COMMENTS

Ticketing Platforms

"It's not just events the airlines do the same thing, if you're on a site looking at something then go back to purchase the prices automatically go up cause they know you're interested. I've bought tickets from different sites and it's ticketmaster that end up sending you the tickets. They are the top mafia in all of this " — storierod

"There is a definite monopoly and domination. However, people are willing to pay exorbitantly for the concert experience, driving prices further upward. If tickets were not purchased, the monopoly would be forced to reduce prices to make sales." — purplesky4jay

Artists

"There's a shared blame, but I blame in order...

1. Artists & venues

2. Buyers seemingly willing to pay any price

3. Ticketing platforms for enabling it

Why do I blame the likes of Live Nation last? Aside from their 15% service fees, they're simply charging what the artists and venues are demanding.

Not part of the topic/discussion, but I'll say it anyway. It's sad that major events are mostly becoming entertainment solely available for the very wealthy. Greed rarely ends well..." — callawayguy

TECHNOLOGY

Apple Names A Hardware Veteran As Its Next CEO

John Ternus, Apple's head of hardware engineering, will become CEO on September 1

Tim Cook departs after 15 years and a remarkable run growing the company's market value

Ternus spent 25 years at Apple and led the transition to in-house Apple Silicon chips

His hardware background raises questions about Apple's

Apple's leadership transition has been anticipated for months, but now that it’s official, it marks a genuine turning point for one of the world's most valuable companies. John Ternus, currently vice-president of hardware engineering, will take the top job on September 1, replacing Tim Cook, who grew Apple from a $350-billion company to one worth roughly $4 trillion US. Ternus has spent his entire career at Apple since joining in 2001, rising through product design and hardware to become one of the company's most prominent public faces at recent product launches.

A Hardware Leader For A Software Moment

Ternus's fingerprints are on some of Apple's most consequential decisions, including the shift to its own silicon chips across all product lines, a move that gave the company greater control over performance and product differentiation. Those who have worked with him describe a collaborative leader who builds strong internal relationships and has earned genuine respect. Tim Cook himself called Ternus "without question" the right person for the role. The open question is whether a hardware-first executive is the right profile for a company that has been visibly struggling to find its footing in artificial intelligence. Apple launched Apple Intelligence in 2024, missed its own target for an AI-powered Siri upgrade in 2025, and has leaned on a partnership with Google's Gemini to fill the gap. That’s an arrangement that creates its own privacy concerns for a company that has long made data security a brand pillar.

What Ternus Inherits

Some analysts argue Apple's hardware-centred identity is actually well suited to the AI era, that no matter how dominant AI becomes, people will need great devices to access it, and Apple builds better devices than anyone. Whether Ternus can extend that argument into a credible AI strategy is the defining challenge ahead.

Read the full story here.

The browser that reads the room before you ask.

Most browsers get you to the page. Norton Neo gets you to the answer. Magic Box understands your intent before you finish typing — no prompting, no switching apps, no copy-pasting. Built-in AI, instantly and for free. Privacy handled by Norton, by default.

THE FEDERAL RESERVE

Powell's Next Move Could Shape The Fed For Years

The Justice Department has stepped back from its criminal probe into Fed headquarters renovations

Powell had vowed to stay until the investigation resolved, now he faces a choice

Trump has threatened to fire Powell and his designated successor Kevin Warsh has a confirmation hearing underway

Markets are watching closely, with Powell's next press conference expected to shed light on his plans

Jerome Powell is likely in the final weeks of his tenure as Federal Reserve chair, and a Justice Department decision Friday has forced a decision. US Attorney Jeanine Pirro announced she was referring the criminal probe into Fed headquarters renovations to the central bank's inspector general, effectively removing the Justice Department from the matter for now. Powell had previously said he would remain at the helm until the investigation was resolved. That condition has now been met, at least partially.

The Decision And What It Means

Powell now faces two paths. He can follow the precedent set by most outgoing Fed chairs and step away when his term as chair expires on May 15, or he can remain as a regular Fed governor through January 2028. Analysts at Evercore ISI suggest the timing of the Justice Department move may have come too late for a clean May 15 exit, and that Powell might choose to stay on for a period to avoid any appearance of leaving under pressure. President Trump has been openly critical of Powell and has threatened to appoint replacements who will cut rates faster. Kevin Warsh, the designated successor, has spoken of a "regime change" at the Fed, and his language and tone have unsettled some observers who value the institution's independence.

Read the full story here.

GLOBAL TRADE & THE ECONOMY

The Strait Of Hormuz And The Recession Question

The US-Israeli conflict with Iran has effectively closed the Strait of Hormuz since late February

About one-fifth of global oil and natural gas supply passes through the waterway

Brent crude is trading around $106 per barrel, roughly 50% above pre-war levels

Economists disagree sharply on recession risk, with duration of the closure the central variable

The closure of the Strait of Hormuz has triggered one of the most significant oil shocks in recent history, and economists are now openly debating whether the disruption is severe enough to push the global economy into recession. The conflict began February 28, and although a ceasefire was extended this week, Iran retains effective control of the strait and the US has mounted a blockade of Iranian ports. The result is a sharp reduction in global oil supply that is being felt from airline fuel costs in Europe to school schedules in Pakistan.

Where Economists Disagree

The central fault line is duration. Major institutions including the OECD and IMF have issued projections that assume a resolution by mid-year, and both see global GDP growth holding reasonably steady at around 2.9% to 3.1%. Critics, though, say those forecasts are too optimistic. Economist Paul Krugman has publicly warned that a full global recession is more likely than not if the strait remains closed for another three months. Oxford Economics has modelled a scenario in which a six-month impasse pushes Brent crude to $190 a barrel and global inflation back toward its 2022 peak, a shock it says would tip the world into outright contraction.

The Stakes For Investors

Oil prices remain elevated but are still below the highs seen after the Russian invasion of Ukraine in 2022, which might give some sense of comfort. But we all know that higher oil prices feed into transportation, food distribution, and manufacturing costs (and many other areas) across every sector of the global economy. Low-income countries and those most dependent on Persian Gulf oil face the steepest exposure. The next few weeks of ceasefire talks will likely determine whether this remains a manageable shock or becomes something more serious.

Read the full story here.

OSFI is where small entrepreneurs’ big dreams go to die

While designed to safeguard the banking system, OSFI’s risk-focused approach is facing scrutiny for its impact on lending to SMEs seeking to grow and expand

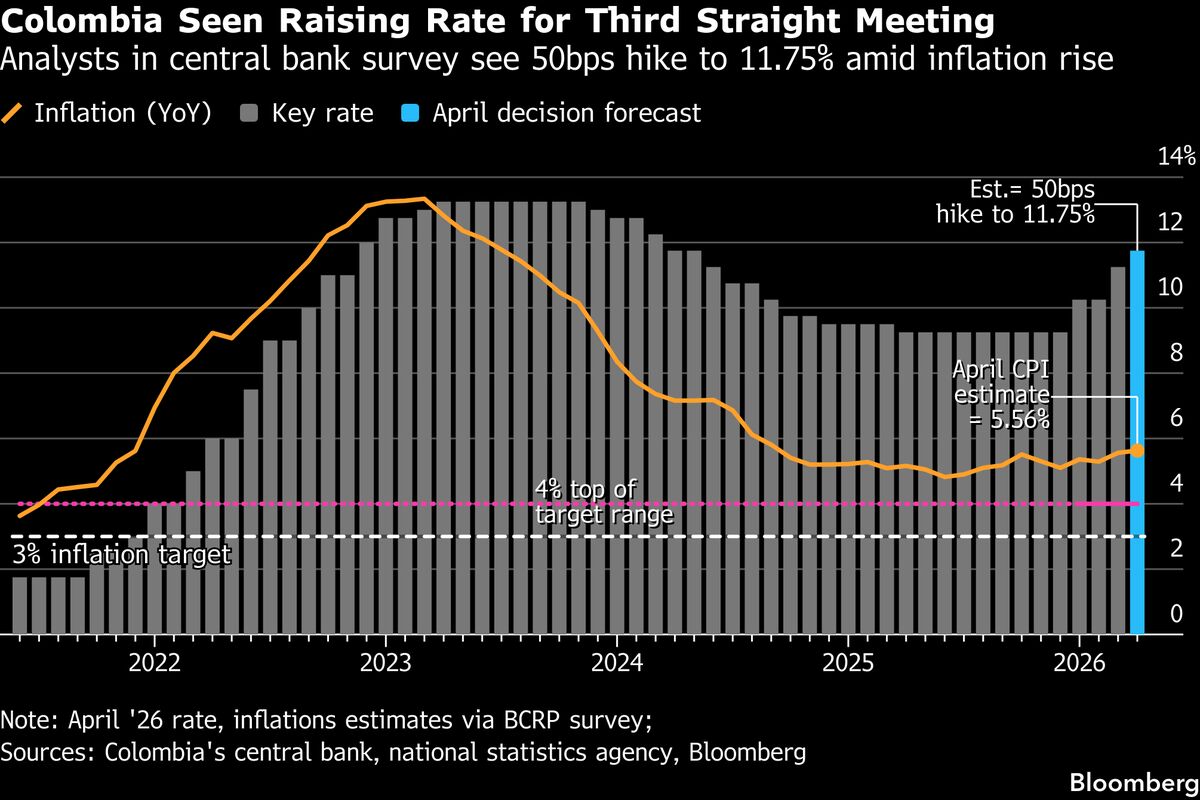

Bank of Canada expected to remain on hold as oil shock reverberates

The central bank is eyeing energy prices warily but are not expected to make any sudden moves

Alberta Energy Regulator orders MAGA Energy to suspend operations over ‘failure to meet its commitments’

The Alberta Energy Regulator has ordered oil and gas firm MAGA Energy Ltd. to suspend its operations over unresolved environmental concerns and non-compliance issues, including unpaid taxes.

Ticketmaster delists Ontario resale tickets after new law caps prices

Ticketmaster has begun delisting resale tickets for Ontario events to comply with a new provincial law that caps the price of such tickets at face value.

Fed Set to Lead Uneasy G-7 With Rates Kept on Hold This Week

Policymakers in the US and across the Group of Seven will probably keep interest rates steady this week while watching nervously for signs of higher energy costs fanning inflation.

History of Presidential Assassination Attempts

In the aftermath of the shooting at the White House Correspondents's dinner, Bloomberg's Joe Mathieu joins David Gura and Christina Ruffini on Bloomberg This Weekend to discuss the history of assassination attempts on US presidents how such events have shaped security protocols in Washington, DC. (Source: Bloomberg)

Higher prices could last for eight months after Iran war, minister says

Officials are monitoring stock levels and planning for any potential disruptions to the supply chain.

China car giant BYD says it can thrive without US

With the price of fuel rising China's BYD says it is positioning itself to benefit from the global shift away from fossil fuels.

Tillis says he's ready to move ahead with confirming Warsh as Trump's pick as Fed chair

The Republican senator who had effectively blocked confirmation of President Donald Trump’s pick to lead the Federal Reserve says he's dropping his opposition after the Department of Justice ended its investigation of the current central bank chair

Photos show China’s automakers unveiling the future of driving at Beijing auto show

China’s top automakers unveil cutting-edge models and technology at the Beijing auto show, highlighting advances in intelligent driving, ultrafast charging and electric vehicles. More than 1,450 vehicles are on display, including 181 global debuts. ___ This is a photo gallery curated by AP photo editors.

Week ending April 24, 2026 | Market Cap > $10 Billion USD

Week ending April 24, 2026 | based on 14-Day RSI | Market Cap > $10 Billion USD

The Relative Strength Indicator (RSI) can provide a signal that suggest a stock is either overbought or oversold.

📈A stock that has an RSI over 70 is considered to be in “overbought” territory. This might suggest that the stock is due for a pullback, however it is not a recommendation to sell.

📉A stock that is trading with an RSI below 30 is considered to be in “oversold” territory. This might suggest that the stock is due for a recovery, however it is not a recommendation to buy. Always perform your own due diligence.

Reply