- The Pulse Newsletter

- Posts

- Americans Haven't Felt This Bad About The Economy Since Ever

Americans Haven't Felt This Bad About The Economy Since Ever

AI cyber risk | Canada's frozen jobs | Live Nation on trial

Marc Beavis

April 12, 2026

In partnership with

Happy Masters Sunday! I’m writing this as we go into what should be and Epic Sunday at The Masters, with at least eleven of the world’s top golfers in contention to make a run for the title, not to mention the $4.5 million prize money. If you’re watching, hope you enjoy!

As for other news this week, the mood among everyday consumers hit rock bottom, a historic low to be exact, and the reasons behind it is as much about geopolitics as it is about economics. We're also looking at a labour market that added jobs on paper but is showing real signs of strain underneath, and a high-stakes legal battle that could reshape how millions of people buy tickets to live events.

My take this week: as is so often the case, the headline numbers are telling one story, but what's underneath them is telling another. Let’s have a look a that gap.

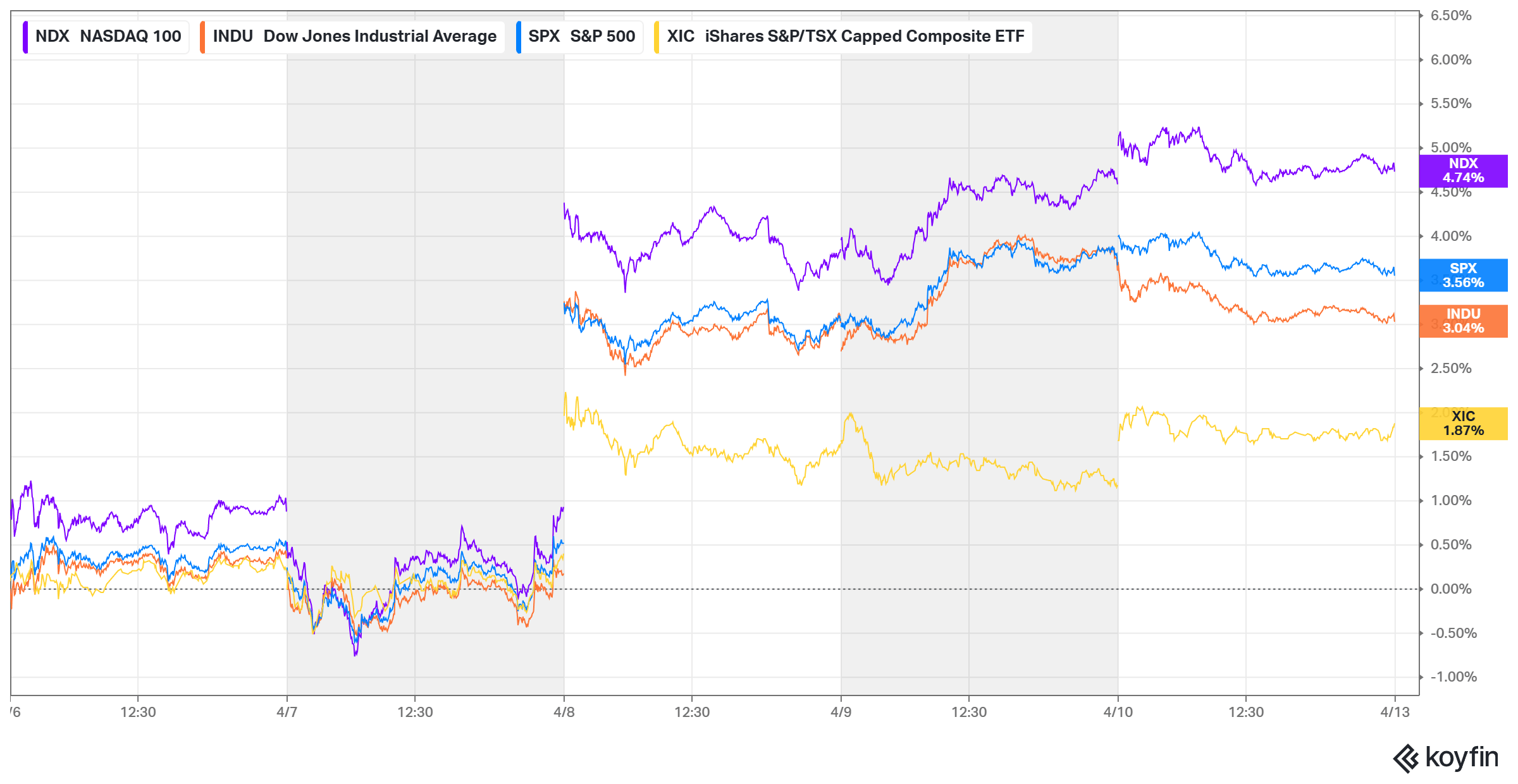

Market Recap: U.S. and Canada

It was another volatile week that ultimately ended in strong positive territory across the board. The markets sold off early, with all four indices pushing into the red by Monday and sliding further through Tuesday morning. Then on Tuesday evening, President Trump announced a two-week ceasefire with Iran. Wednesday opened with a sharp relief rally, drove every index up, and the gains held through the rest of the week. The recovery was broad-based and decisive, with technology leading the charge.

As for the numbers, the Nasdaq 100 led the group with a weekly gain of +4.74%. The S&P 500 followed at +3.56%, with the Dow Jones close behind at +3.04%. The TSX lagged the US indices but still finished the week solidly in positive territory, up 1.87%.

Week ending April 10, 2026

Major Economic Stories This Week

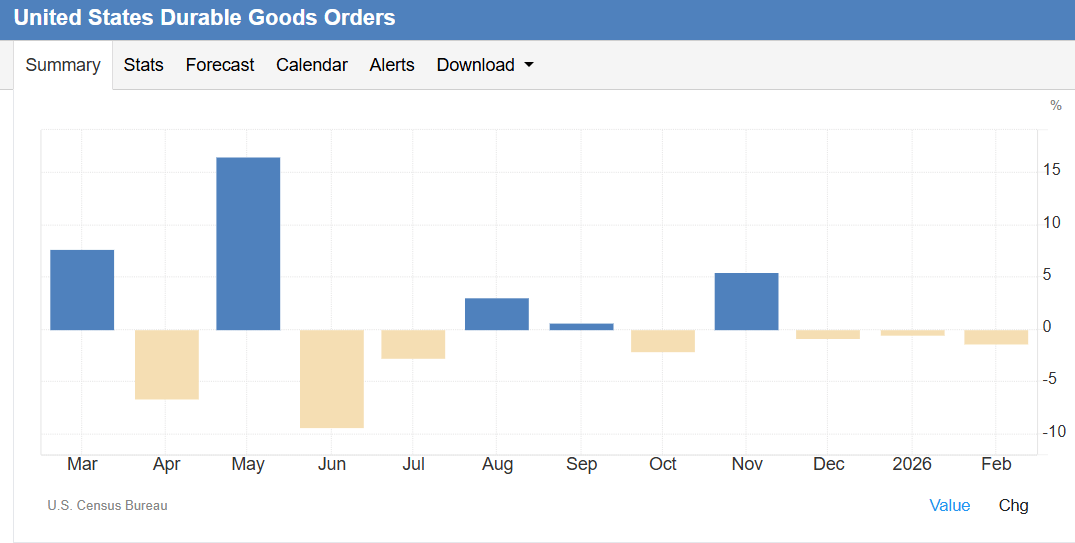

US Durable Goods Orders Extend Decline

New orders fell 1.4% in February to $315.5 billion, the third straight monthly decline.

In this report, the headline looks worse than the underlying story. Transportation equipment drove nearly all of the weakness, with nondefense aircraft orders plunging 28.6%. This is a notoriously volatile category that can swing monthly figures dramatically in either direction. Strip that out and orders actually rose 0.8%, with machinery up 1.5% and primary metals gaining 2.2%.

What we see is a headline number getting distorted by a single volatile input. For investors watching industrial exposure, the underlying trend still points to stable demand rather than broad deterioration.

Prior month revised to -0.5% — headline decline is now part of a three-month downward sequence

Nondefense aircraft: $19.2 billion — the category alone responsible for distorting the headline

Defense capital goods and core capex orders: held relatively stable, no broad pullback in business investment

February marks the weakest three-month stretch for total orders since mid-2023

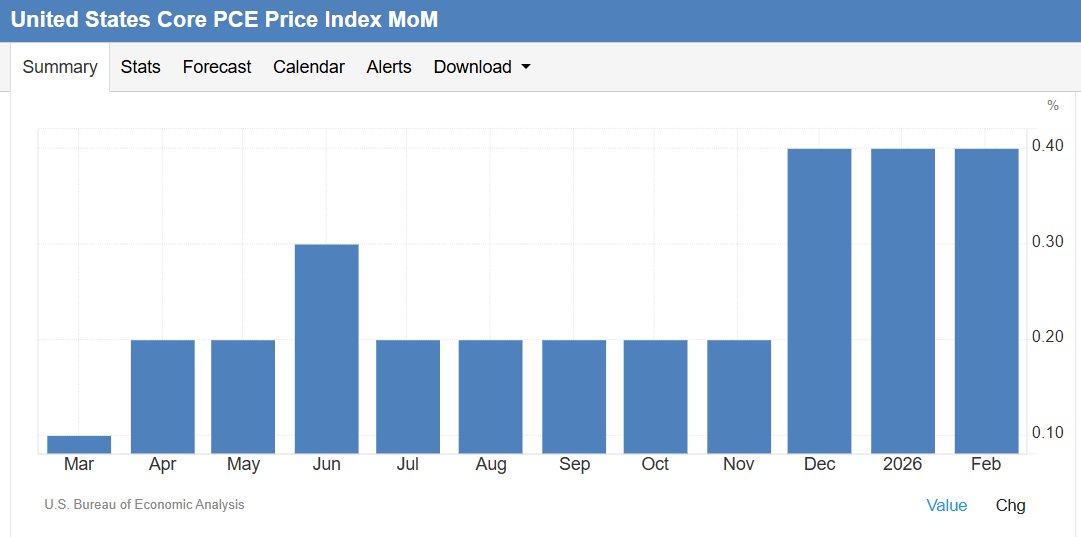

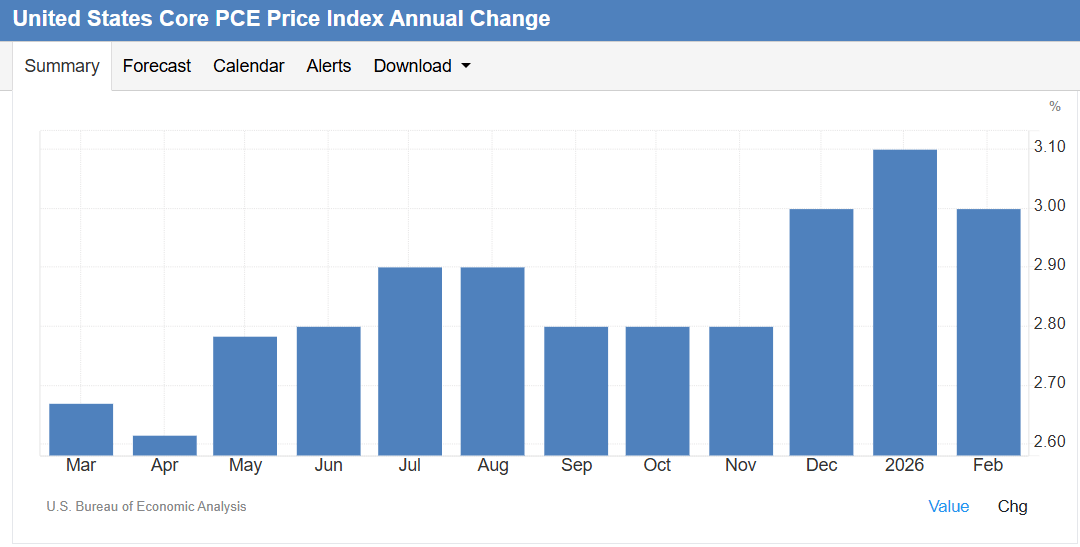

Core PCE Holds At A 10-Month High

The Fed's preferred inflation measure rose 0.4% month-over-month in February for the third consecutive month, with annual core PCE at 3.0%.

Three months in a row at 0.4% monthly is officially a trend. Annual core PCE edged down slightly from 3.1% but remains well above the Fed's 2% goal, and the result came in exactly where markets expected, and as we would expect, we saw little reaction.

What matters most here is the persistence of monthly gains. If this pace holds through spring, the conversation shifts from "when do cuts start" to "whether cuts happen at all this year." The Fed has been patient, too patient for some, and this data gives them every reason to stay that way.

Services inflation: primary driver of persistence; goods prices remain comparatively contained

Core PCE has now run above 2.5% annually for 36 consecutive months

Personal income and spending data released alongside: consumption held firm in February

Fed's next meeting: no rate move expected; market odds of a 2026 cut have fallen below 50%

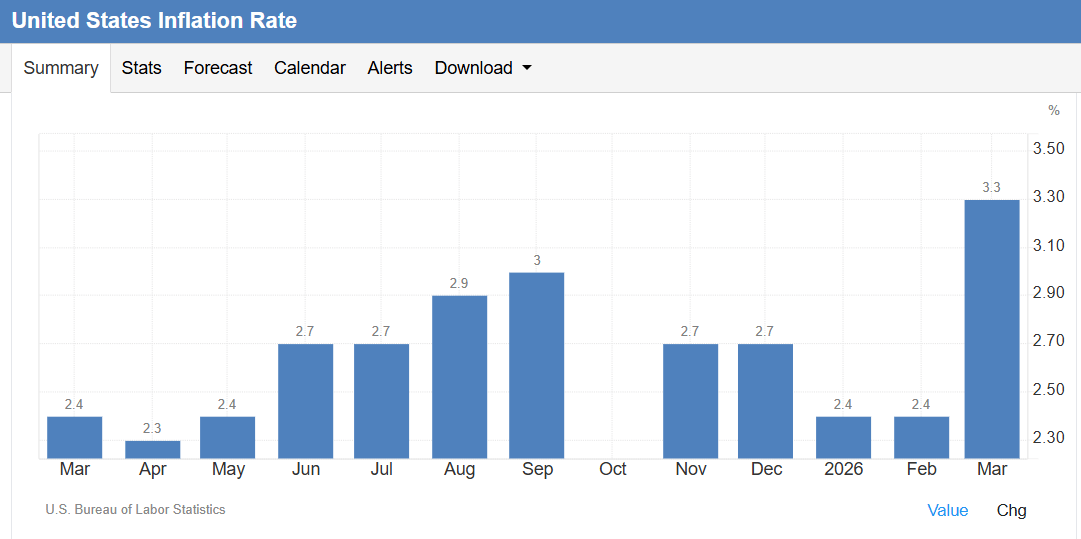

An Energy Shock Rewrites The US Inflation Story

US headline CPI spiked 0.9% in March, the largest monthly gain since June 2022, pushing the annual rate to 3.3%, the highest since May 2024.

What we have is an energy story, not a demand story, and that distinction matters. The Iran conflict drove a sharp spike in fuel costs that accounts for the bulk of the monthly move, with gasoline jumping 21.2% and fuel oil up a huge 44.2%. Remove that from the equation and the picture is far more contained.

Core inflation, which strips food and energy, came in at 2.6% annually and just 0.2% for the month, both at or below expectations. Services inflation remains firm, with transportation services at 4.1% and shelter holding at 3.0%. Used vehicles continued their deflationary trend, down 3.2%. The Fed can read this print and know the source, but they still can't cut rates into a 3.3% headline number with inflation expectations on the rise. The discrepancy essentially freezes monetary policy in place.

Annual headline CPI: jumped from 2.4% in both January and February to 3.3% in March — the sharpest two-month acceleration in over a year

Fuel oil: +44.2% for the month — the single largest contributor after gasoline

Apparel: +3.4% annually — adding modest upward pressure on the goods side

Medical care services: +3.7% annually — a category worth watching as a secondary inflation driver

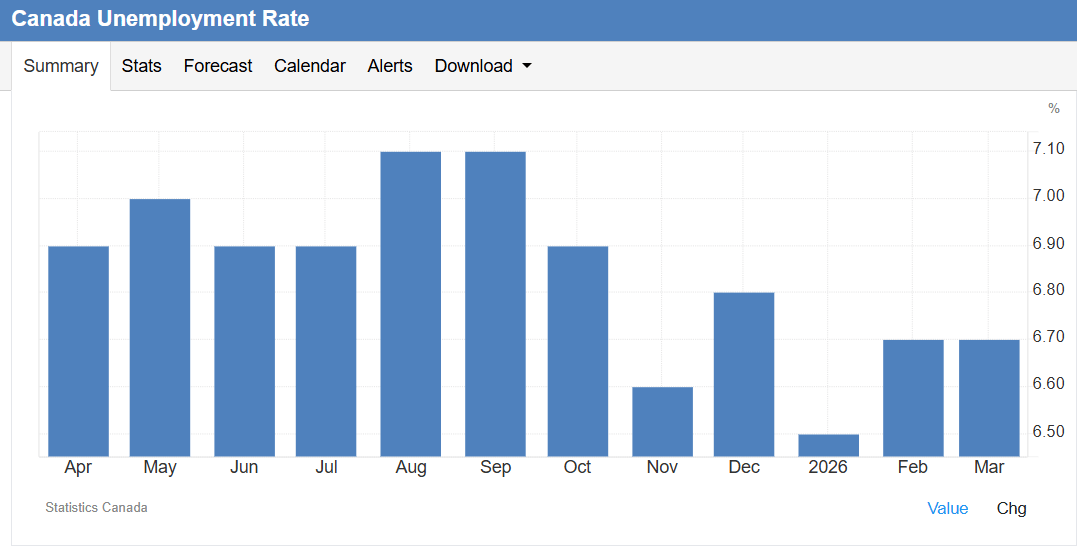

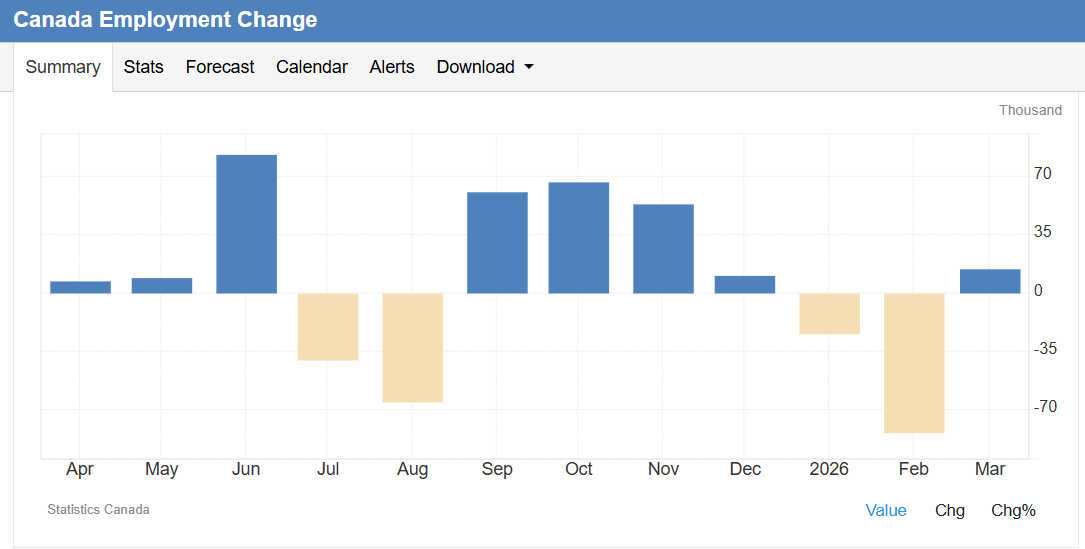

Canada's Labour Market Is Frozen In Place

Employment rose 14,100 in March, ending a two-month losing streak, while the unemployment rate held at 6.7%.

After February's 84,000-job loss, any positive number was going to look like relief, and the headline does offer that. But looking at where the jobs actually come from tells a more cautious story. Full-time employment declined on the month, meaning the net gain came 100% from part-time positions. That’s bad news because part-time work doesn't generate the same income stability or spending confidence as full-time employment.

The unemployment rate came in slightly below the expected 6.8% and remains well off its August 2025 peak of 7.1%, so that tells us the market isn't falling apart, but it isn't recovering either. Participation and employment rates were both flat. Core-age unemployment held at 5.8%, youth unemployment stayed high at 13.8%, and the labour market overall looks less like a recovery and more like a system that has simply stopped moving.

Number of unemployed: rose by 1,000 on the month — marginal but moving in the wrong direction

Workers aged 55 and older: unemployment held at 4.9% — the most stable cohort in the market

Wage growth: +3.5% annually — exceeds inflation near 2%, keeping real wages modestly positive for now

Job gain of 14,100 came in just below the forecast of 15,000 — a small miss but directionally in line

TOP INSIGHTS

The Iran Conflict Has Done What Tariffs Could Not, Broken Consumer Confidence

What stands out this week isn't the CPI number, it’s the sentiment collapse happening alongside it. Tariffs rattled markets and generated plenty of headlines, but much to most people’s surprise, consumers largely kept spending through that period. The Iran conflict appears to be hitting differently. The University of Michigan's sentiment index has dropped to its lowest point ever recorded, and the big concerns are the gas prices people can see every time they fill up. That's a more immediate and visceral economic signal than a trade dispute.

If we look at the everyday household, the math is simple: higher fuel costs reduce discretionary income before anything else adjusts. Gasoline isn’t optional for most Canadian and American families. When it jumps 21% in a month, it crowds out spending in other areas, such as restaurants, retail, entertainment. You get the picture. That reduction in spending eventually shows up in revenue, then earnings, then hiring decisions.

I think the ceasefire, as fragile as it is, gives the next sentiment reading a reasonable chance of recovering. But inflation expectations, especially the longer-term ones, tend to be stickier than the headline index. If those stay elevated into May, the Fed faces a credibility problem that goes beyond any single data release. Watch the May sentiment print closely. That one will matter more than this one.

Canada's Jobs Story Is About Who Is Hiring, Not How Many

The headline employment gain is real, but it's worth understanding what's actually driving it. The sectors showing consistent strength over the past year are public administration, healthcare, education, and professional services, all of them either government-funded or largely insulated from private sector demand cycles. Manufacturing shed 44,000 jobs compared to a year ago. Retail and wholesale are soft. The private sector is being carried by the public one, and that matters for a few reasons. Government hiring tends to be countercyclical and budget-constrained, not demand-driven. It provides stability, but it doesn't signal that businesses are confident enough to expand headcount. A household whose primary earner works in manufacturing or retail is experiencing a very different labour market than the aggregate number would suggest. Part-time job gains help, but they don't close that gap.

Here's what I'm watching: wage growth at 3.5% currently exceeds inflation near 2%, which means real wages are modestly positive and workers are nominally keeping ahead of prices, at least for now. But if Iran-driven price increases filter into Canadian consumer prices, and they will, that calculation flips. Real purchasing power will compress just as the labour market is already showing softness. That combination gives the Bank of Canada more reason to cut, not less. I'd expect the next move to come earlier than the market is currently pricing.

The Fed Is Caught Between A Supply Shock And Its Own Credibility

This week’s U.S. inflation numbers present the Fed with a genuinely uncomfortable situation. Core PCE has been running at 0.4% monthly for three straight months, headline CPI just printed 0.9% for a single month, and inflation expectations are rising. On every metric that matters for the Fed's mandate, the data argues for holding rates, possibly for the rest of the year.

And yet the source of most of this pressure is a geopolitical shock the Fed has no tools to address. Monetary policy can’t lower gas prices. It can’t resolve a conflict in the Middle East. Raising rates would slow demand even more, without touching the supply-side problem that's actually driving prices higher. The Fed knows this, but they also know that cutting into a rising inflation environment, even a supply-driven one, risks embedding higher expectations into wages and contracts, which is how temporary shocks morph into structural ones.

This is the dilemma. The right economic response might be to look through the energy spike and hold steady with a bias toward easing as the shock fades. But the credibility cost of appearing to tolerate inflation above target, especially with long-term expectations already drifting higher, is real. My take is that the Fed holds through mid-year at minimum, communicates patience without making a firm commitment, and hopes the ceasefire holds long enough for energy prices to give them some cover. Cuts in 2026 are still possible, but they're no longer probable.

The 10 Best AI Stocks to Own in 2026

AI is moving from experiment… to essential.

Every major industry is integrating it.

Every major company is investing in it.

By late 2025, AI was already an $800B market — growing at a pace that could push it well beyond $1 trillion in the years ahead.

Cloud infrastructure is scaling fast.

AI-enabled devices are multiplying.

Automation is becoming standard.

But here’s the real question…

When trillions flow into this transformation — which stocks stand to benefit most?

Our new report reveals 10 AI stocks positioned across the backbone of this shift — from the companies powering the infrastructure… to those embedding intelligence into everyday systems.

If you want exposure to one of the defining growth trends of this decade, start here.

TOP STORY

US Consumer Confidence Hits An All-Time Low

Sentiment index falls to 47.6, lowest ever recorded

Iran conflict cited across all income, age, and political groups

One-year inflation expectations jump a full percentage point

Ceasefire announcement came after most responses were collected

American consumers are more pessimistic about the economy than at any point in the post-war era, lower than during the 2008 financial crisis, lower than during the pandemic, and lower than during the worst of the 2021-2022 inflation surge. Let that sink in for a minute.

The University of Michigan's April sentiment reading came in at 47.6, an 11% drop from March, with respondents across every demographic group pointing to the US-Israeli conflict with Iran as the primary driver of their anxiety. One-year inflation expectations jumped a full percentage point to 4.8%, the largest single-month increase in a year, while longer-term expectations rose to 3.4%, the highest since November. The only caveat: nearly all responses were collected before President Trump announced a ceasefire with Iran earlier this week, which may soften the next reading.

Why Spending May Hold, For Now

The critical question isn't whether consumers feel bad, it's whether they act on it. Consumer spending accounts for roughly two-thirds of the US economy, and historically, pessimism alone hasn't always translated into cutbacks, particularly when the labour market stays intact. Unemployment remains at 4.3%, and new jobless claims suggest companies are still holding on to workers. Generally speaking, as that as long as paycheques keep coming, spending tends to follow, even through periods of low confidence.

The Risk That Changes Everything

The big concern is what happens if sentiment-driven caution combines with rising unemployment. Economists broadly agree that a deteriorating jobs market would force households to pull back sharply, especially with inflation expectations already elevated and gas prices squeezing budgets at the pump. As I noted above, the ceasefire is fragile, and analysts expect further soft readings ahead if the conflict remains unresolved.

Read the full story here.

American consumer confidence just hit its lowest point in recorded history. Lower than during the financial crisis and even lower than during the pandemic. That kind of reading tends to generate a lot of noise, but what matters for investors is what it actually signals about where the economy is heading.

Please vote on this week's question:

What does record-low consumer sentiment signal to you? |

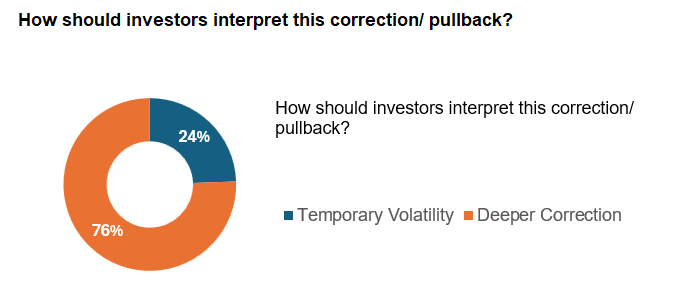

LAST WEEK’S POLL RESULTS

Last week I asked how investors should interpret the recent market correction and pullback. A decisive 76% said they view it as a deeper correction, while just 24% saw it as temporary volatility. Thanks to everyone who voted.

TOP COMMENTS

Deeper Correction

"A sustained disruption or instability in the Strait of Hormuz would keep oil prices structurally elevated, especially given limited spare capacity and already-depleted buffer reserves. Prolonged energy price strength would likely reaccelerate inflation, complicating the Federal Reserve’s path to easing.

In that scenario, the Fed would be forced to keep rates higher for longer or potentially hike further, tightening financial conditions. This would weigh on equity valuations and liquidity, increasing the probability of a broader market drawdown." — shaneachung

"Everywhere troubling events do not allow me to buy any large purchases. Many people I know feel the same. A hold pattern for me." — len.short.4

"I'm taking the people over the data when it comes to the economy, which eventually bleeds into the market.

I read something earlier today that really jumped off the page at me. "Over the last year, 40% of those switching jobs took pay cuts of 10% or more" (some a lot more), according to a new analysis by Revelio Labs. That’s a shift I don’t think the economy saw coming and if the data can be trusted, the ramifications of less spending power should show in the coming months economic data. TBD..." — callawayguy

"The bull market has reached the end of its historical run, and the economic cycle has been overdue for a pause. Yet, optimism fueled by AI spending has kept it going. Market volatility, rising energy prices, conflict in the Middle East, and ongoing trade uncertainty will ultimately serve as the catalysts that dislodge the pebble holding the boulder. Once that shift begins, the movement will be swift." — alir.mortazavi

"The Iran war is going to make everything worse for a long time; longer than the war actually lasts, I think." — mrrobpog

"With no US exit plan and Israeli thirst for war, it is inevitable that businesses will be cautious on investments, will be impacted by stalls in the supply chain and impact on margins and growth. I'm a retiree who is still too young to receive the state pension. My paper loss already is giving me sleepless nights but I'll try to hang tight and pray for a solid, swift diplomatic solution." — skarkez

ARTIFICIAL INTELLIGENCE

Canadian Banks And Regulators Meet Over Anthropic's New AI Model

Canadian Financial Sector Resiliency Group convened Friday to assess risks

Anthropic's Mythos model can identify vulnerabilities in major operating systems

US Treasury held a parallel meeting with America's largest bank CEOs

Model not released publicly, limited preview shared with critical infrastructure firms

Canada's top banking executives and financial regulators gathered Friday to assess the cybersecurity risks posed by Anthropic's newly revealed AI model, known as Mythos. The meeting of the Canadian Financial Sector Resiliency Group, chaired by the Bank of Canada's chief operating officer and including representatives from the Department of Finance, OSFI, and Canada's six largest banks, was called as a situational awareness exercise, not an emergency response. It followed a similar meeting held earlier in the week in the US, where Treasury Secretary Scott Bessent convened the CEOs of America's largest financial institutions alongside Federal Reserve chair Jerome Powell. Anthropic has described Mythos as capable of identifying thousands of software vulnerabilities across every major operating system and web browser, a capability it says can be used both defensively and offensively.

What Makes This Model Different

Anthropic chose not to release Mythos to the general public. Instead, a preview version has been made available through a program called Project Glasswing to a select group of organizations with critical digital infrastructure roles, including Amazon, Microsoft, Apple, Google, JPMorganChase, CrowdStrike, and Nvidia. The concern among regulators isn't just what Mythos can do in the right hands, it's what it enables in the wrong ones. Cybersecurity experts note the model can identify patterns in flawed code faster than any human analyst, and by some estimates there are trillions of lines of problematic code across existing systems.

Where Regulators Stand

OSFI said it has no plans for short-term changes to its existing guidelines but is in active conversations with institutions to assess the situation. Canada's banks, for their part, say they already manage AI-related risks through established internal frameworks and regulatory requirements. Whether those frameworks were designed with a tool of this capability in mind is a different question.

Read the full story here.

EMPLOYMENT

Canada's Job Market Is Stuck, Not Recovering

March added 14,000 jobs, ending a two-month losing streak

Gain driven by part-time work as full-time positions showed little change

Manufacturing down 44,000 jobs compared to a year ago

Public sector described as the primary force holding the market together

Canada's labour market technically improved in March, 14,000 jobs were added and the unemployment rate held at 6.7%, but economists aren't calling it a recovery. The phrase appearing over and over in analyst commentary is "frozen." Labour force growth has stalled, immigration-driven supply has slowed, and the structural slack built up over the past year hasn't cleared. The job gain ended a two-month losing streak that included February's steep 84,000-job loss, but the composition of the March numbers doesn’t do much to suggest any real underlying momentum. Part-time positions drove the gain while full-time employment showed little change, and the sectors leading the market are public administration, healthcare, and education, not private employers responding to demand signals.

Where The Weakness Is Concentrated

Manufacturing shed 44,000 jobs compared to the same month last year, with US tariff exposure cited as a contributing factor. Retail and wholesale also declined, which analysts flagged as particularly concerning given those sectors track consumer demand closely. Youth unemployment held steady at 13.8% following a sharp rise in February, and core-age unemployment was unchanged at 5.8%. Wage growth at 3.5% is ahead of inflation near 2%, and that has kept real purchasing power marginally positive, although that buffer narrows quickly if Iran-driven price increases reach Canadian consumers.

The Outlook

Economists will be watching to see whether the labour market's stall becomes a slide. The public sector's stabilising role has limits, government hiring has slowed, and the private sector isn't filling the gap. With tariff pressure ongoing, immigration-driven labour supply reduced, and a potential commodity price shock on the horizon, the conditions for a genuine recovery aren't in place just yet.

Read the full story here.

MONOPOLIES

Live Nation Faces Jury In Landmark Antitrust Trial

34 states allege Live Nation and Ticketmaster monopolise the concert industry

States claim the company controls 86% of the concert market

Live Nation argues success is not the same as illegal monopoly behaviour

Federal government settled separately last month after winning key concessions

Jury deliberations are underway in Manhattan federal court in a civil antitrust case that could reshape the live entertainment industry. Thirty-four states have brought the case against Live Nation Entertainment and its ticketing subsidiary Ticketmaster, arguing the company has used its dominant position to crowd out competition and drive up prices for fans. The case follows a five-week trial and picks up where the federal government left off. Last month, the Justice Department settled separately after securing concessions related to ticket sales at dozens of Live Nation amphitheatres.

What The States Are Arguing

The states contend that Live Nation controls 86% of the concert market, or 73% of the broader live events market when sports are included. Their closing argument framed the case as a straightforward market dominance issue that sees one company controlling venues, promotion, and ticketing simultaneously in a way that leaves artists, fans, and competing promoters with few alternatives.

Live Nation's Defence

Live Nation's legal team acknowledged the company's scale but pushed back on the characterisation of its behaviour as anti-competitive. Their argument: being the biggest player in an industry isn't illegal. The company contends there is more competition in live entertainment today than ever before, and that its growth reflects consumer demand and business performance rather than exclusionary conduct. There’s no doubt the outcome of these deliberations will have significant implications for how the live events industry is structured going forward.

Read the full story here.

Iran still controls the Strait of Hormuz, and nothing will ever be the same again

The war has changed the complexion of the global energy equation, with Iran emerging as the new pivot in the emerging new order

The untold danger of unchecked capitalism

Economic policy often assumes that individuals are rational, emotionless actors - but people don’t always behave the way markets expect them to

In a new CUSMA, should Canada offer the U.S. stronger energy rights?

With the future of free trade between Canada and the United States unclear at best, a look to the past could provide hints at where critical exports of energy fit into a deal in the future.

A novelist was accused of using AI. Why the literary world is still grappling with guardrails

The recent cancelling of a horror novelist's book demonstrates the conundrum that literary professionals face as they comb through every pitch, query letter and manuscript lobbed their way: how do you separate the proverbial wheat from the AI-generated chaff, and what happens if you get it wrong?

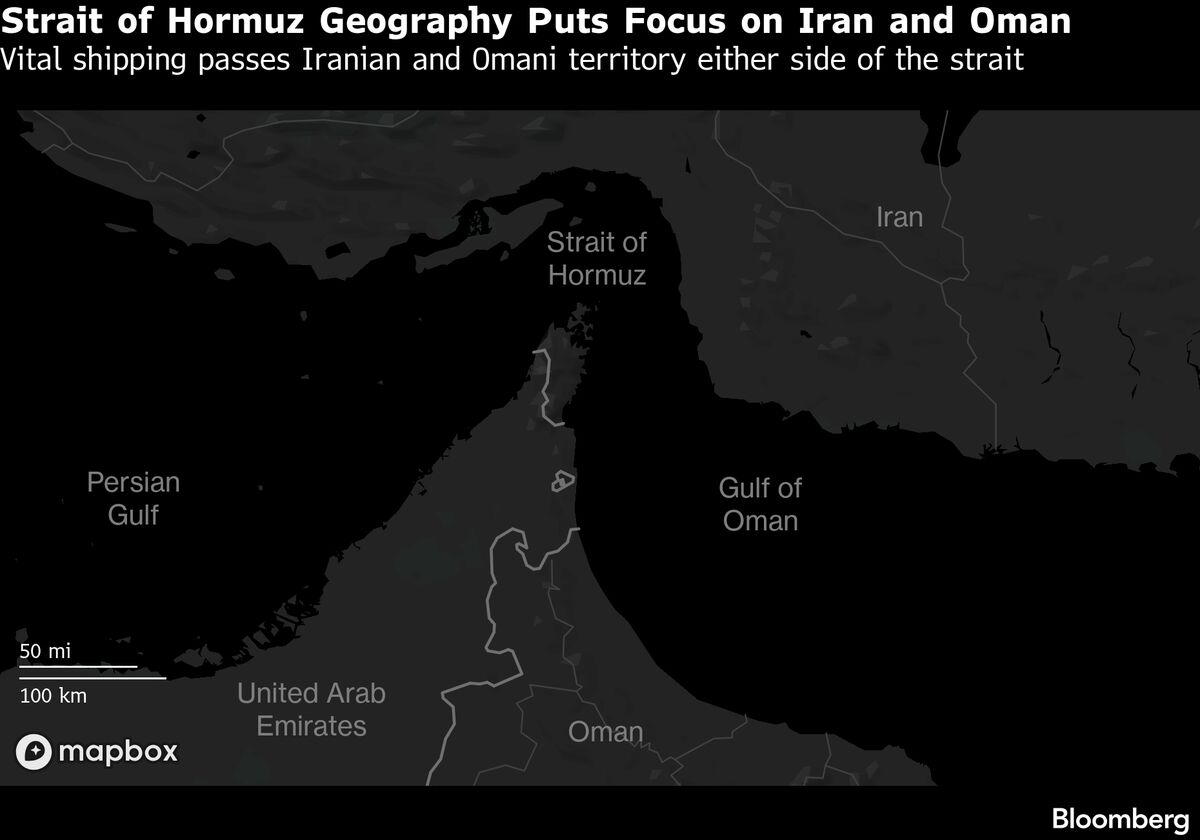

Trump Says US to Seal Hormuz Strait, Severing Key Iran Lifeline

President Donald Trump said the US will blockade the Strait of Hormuz following the failure of peace talks with Iran in Islamabad this weekend, a move that will likely exacerbate oil and fuel shortages globally.

Author Arthur Shipnuck Talks New Rory McIlroy Book

Author Alan Shipnuck joins Christina Ruffini and Tim Stenovec on Bloomberg This Weekend to discuss his new biography, 'Rory: The Heartache and Triumph of Golf's Most Human Superstar,' that offers insight into the superstar's complex career and personal struggles. Watch the show LIVE every Saturday and Sunday morning. (Source: Bloomberg)

White House staff told not to place bets on prediction markets

The gambling platforms have grown in popularity, with some users making wagers on conflicts.

Great at gaming? US air traffic control wants you to apply

A new government ad campaign is trying to persuade gamers to apply for air safety roles.

Buyers fret as the average cost of a new car nears $50K

Vehicle ownership has long been a big part of the American dream

Judge rejects bid to stop Arizona’s prosecution of Kalshi on wagering charges

A federal judge has denied a bid by prediction market operator Kalshi to bar Arizona prosecutors from moving forward with a criminal case against the company

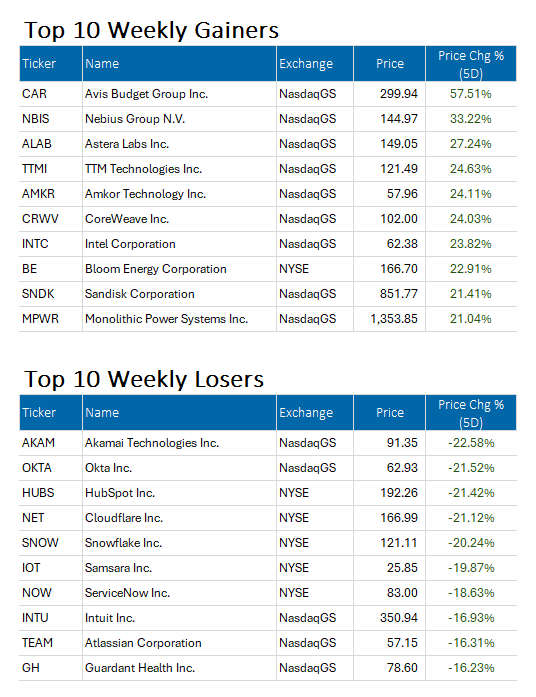

Week ending April 10, 2026 | Market Cap > $10 Billion USD

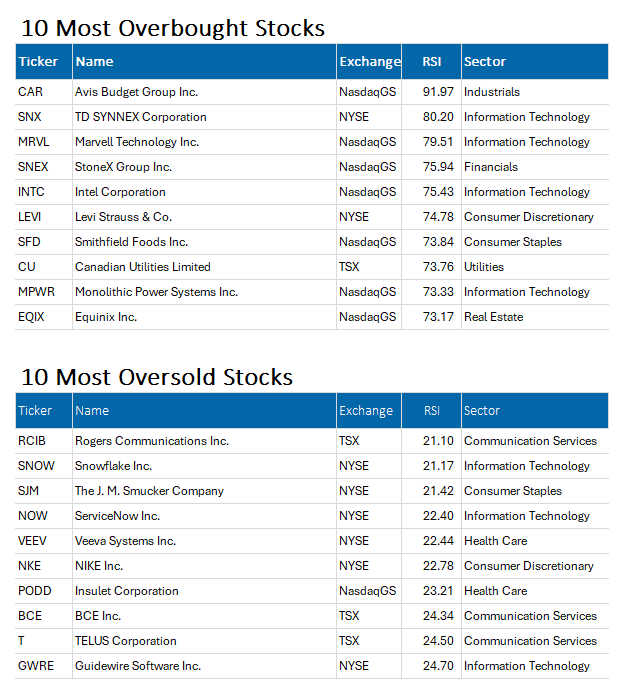

Week ending April 10, 2026 | based on 14-Day RSI | Market Cap > $10 Billion USD

The Relative Strength Indicator (RSI) can provide a signal that suggest a stock is either overbought or oversold.

📈A stock that has an RSI over 70 is considered to be in “overbought” territory. This might suggest that the stock is due for a pullback, however it is not a recommendation to sell.

📉A stock that is trading with an RSI below 30 is considered to be in “oversold” territory. This might suggest that the stock is due for a recovery, however it is not a recommendation to buy. Always perform your own due diligence.

Reply